In recent weeks, insurers in many areas of the country have unveiled the premiums they propose to charge for individual market health insurance policies in 2019. In setting premiums for 2019, insurers are taking account of several policy changes that will be newly in effect for the 2019 plan year, including repeal of the individual mandate penalty and Trump Administration actions to expand the availability of plans that are exempt from various Affordable Care Act (ACA) requirements. These policy changes are generally expected to cause many healthier people to leave the individual market and thereby raise individual market premiums.

In “How Would Individual Market Premiums Change in 2019 in a Stable Policy Environment?,” Matthew Fiedler examines how premiums would change in 2019 absent these looming policy changes. Drawing on a range of data sources, Fiedler first estimates how insurers are performing in the ACA-compliant individual market in 2018, and then uses those estimates to evaluate how premiums would change in 2019 in a stable policy environment. The analysis reaches two main conclusions:

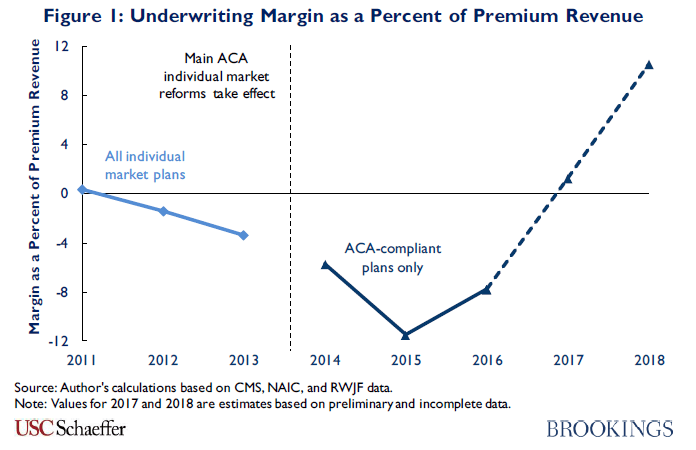

- Insurers will earn large profits in the ACA-compliant individual market in 2018: Fiedler projects that insurers’ revenues in the ACA-compliant individual market will far exceed their costs in 2018, generating a positive underwriting margin of 10.5 percent of premium revenue, as illustrated in Figure 1 of the paper. This is up from a modest positive margin of 1.2 percent of premium revenue in 2017 and contrasts sharply with the substantial losses insurers incurred in the ACA-compliant market in 2014, 2015, and 2016. The estimated 2018 margin also far exceeds insurers’ margins in the pre-ACA individual market. These estimates for 2018 as a whole are broadly consistent with the results of a recent analysis of individual market insurers’ financial results for the first quarter of 2018 recently published by researchers at the Kaiser Family Foundation.

The estimated improvement in insurers’ margins for 2018 is driven by the substantial premium increases insurers implemented for 2018, which will almost certainly be more than sufficient to offset the loss of cost-sharing reduction payments and what appears likely to be another year of moderate growth in underlying claims spending. Prior analysis of insurers’ 2018 rate filings suggests that many insurers expected policy changes that are now scheduled to take effect in 2019, notably repeal of the individual mandate penalty, to take effect in some form during 2018, which may have led insurers to incorporate those policy changes into their premiums a year early.

- In a stable policy environment, average premiums for ACA-compliant plans would likely fall in 2019: Fiedler’s analysis defines a “stable policy environment” as one in which the federal policies toward the individual market in effect at the start of 2018 remain in effect for 2019. Notably, this scenario assumes that the individual mandate penalty and limits on short-term, limited duration insurance policies remain as they were at the start of 2018, but does not assume the reversal of policy changes that were already in place at the start of 2018, like the end of CSR payments. Under those circumstances, insurers’ costs would rise only moderately in 2019, primarily reflecting normal growth in medical costs. Meanwhile, for reasons discussed in detail in the paper, it is unlikely that insurers would set 2019 premiums with the goal of keeping margins at their unusually high 2018 level. Downward pressure on premiums from falling margins would likely more than offset upward pressure on premiums from underlying cost pressures, so premiums would fall on net.

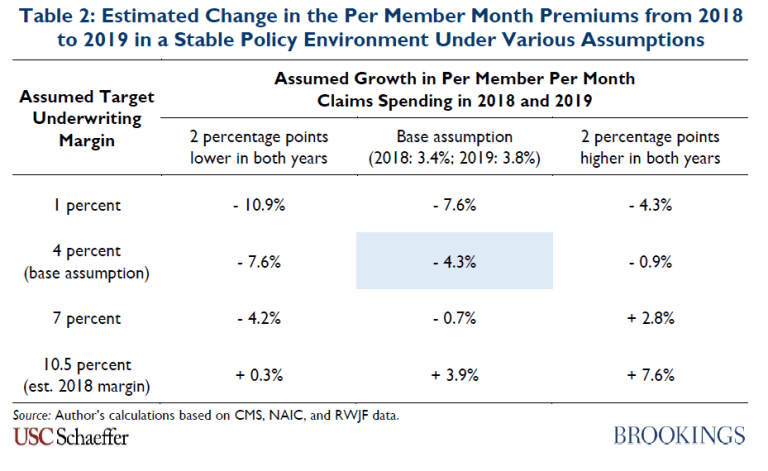

Indeed, Fiedler’s base assumptions imply that the nationwide average per member per month premium in the individual market would fall by 4.3 percent in 2019 in a stable policy environment, as shown in Table 2 of the paper. This estimate is subject to some uncertainty, primarily because of uncertainty about underlying individual market claims trends and about the margins insurers are likely to target for 2019. However, Fiedler estimates that average premiums would decline in a stable policy environment under a range of plausible alternative assumptions.

Download the full report: How Would Individual Market Premiums Change in 2019 in a Stable Policy Environment?.

Editor’s Note: This analysis is part of the USC-Brookings Schaeffer Initiative for Health Policy, which is a partnership between the Center for Health Policy at Brookings and the University of Southern California Schaeffer Center for Health Policy & Economics. The Initiative aims to inform the national health care debate with rigorous, evidence-based analysis leading to practical recommendations using the collaborative strengths of USC and Brookings.

You must be logged in to post a comment.