Social Security was developed to ensure financial security for workers and their families in old age based on their work history. In theory, there are pension system incentives in place to influence when a worker chooses to retire (e.g., Gruber and Wise, 2004). For instance, while individuals can claim their Social Security retirement benefit at age 62 (the Early Eligibility Age), delaying claiming benefits beyond that age leads to increases in the benefit amount until age 70, at which point the benefit increases stop. However, in practice, the majority of people claim their Social Security retirement benefits sooner than would be optimal to their financial wellbeing in old age (Shoven and Slavov, 2014).

A major feature of Social Security in the U.S. are auxiliary benefits – benefits paid to someone other than the worker – typically a spouse, survivor, or child. These are benefits the spouse may be entitled to after the worker retires and, in the case of survivor benefits, after his or her death. These benefits may top up the spouse’s/survivor’s own benefits. As is the case with retirement benefits, survivor benefits also provide significant incentives for delayed claiming by the worker and spouse. However, spousal benefits encourage earlier claiming by the worker as they cannot be paid until a worker claims his or her retirement benefit, meaning a year’s delay in claiming also leads to a year’s delay in the worker’s spouse receiving the spousal benefit.

In our recent working paper, we characterize the complex interaction of worker and spouse incentives and investigate whether an additional dollar of benefit paid to a worker’s spouse or survivor is valued the same as an additional dollar of benefit paid to the worker. If households pool resources and Social Security income goes into a joint account, then arguably who the benefit is paid to should not matter. However, if workers do not understand the existence or incentives of these benefits, or if they discount spousal income relative to their own, then it is possible that an additional dollar of spouse or survivor benefits is valued less than an additional dollar of one’s own Social Security benefit.

How big are the incentives to delay claiming for spousal or survivor benefits?

The gains depend on a worker and spouse’s earnings history. Spousal benefits, equal to the better of 50% of the worker’s benefit or the spouse’s own benefit, can only be collected once the worker has claimed his or her own benefit and are only increased for delayed claiming between age 62 and the person’s full retirement age (i.e. 65-67 depending on year of birth), rather than age 70. That design significantly reduces the benefits to delayed claiming.

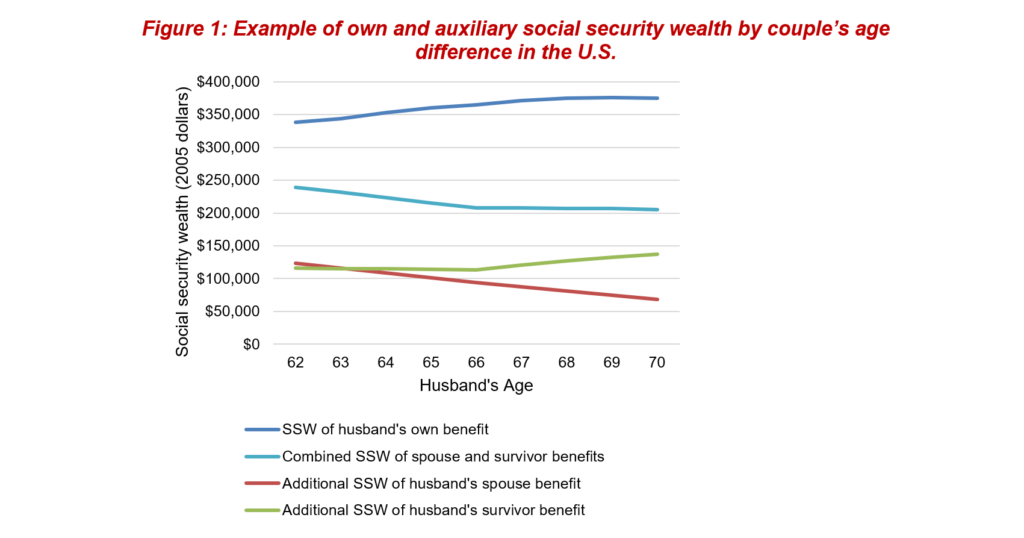

Survivors are entitled to the better of 100% of the worker’s benefit or their own benefit and are increased if the worker delays claiming up until age 70. Figure 1 shows, for each benefit type, the social security wealth by claiming age (i.e., the present value of lifetime social security benefits accounting for mortality) for a worker who is a sole earner (we give the example of a male sole earner as gender-based mortality influences the value of these benefits and men are typically the sole earner in such households). Spouse and survivor benefits for this single-earner household are large, peaking at 71% of the value of own benefits at age 62. Dual-income households benefit less, and a dual-income household with equal earnings histories would not benefit at all, from spouse and survivor benefits (not pictured).

Notes: Hypothetical example based on future claiming decisions of a household where the primary earner is a male, age 60 in 2005 and has an earnings history where he would be entitled to a $2,000 monthly benefit at his FRA (age 66) and where his wife, same age, has no entitlement based on her own earnings history. Inflation is assumed to reflect CPI-W through 2020 and remain constant at this value beyond 2020 (1.3%). The real discount factor is assumed to be one (i.e., no real discounting). Mortality rates are based on age and gender and reflect cohort mortality rates through 2018, and then assume 2018 period life table rates beyond 2018.

Our main finding is that the worker’s decision to continue working does not respond to claiming incentives built into spousal and survivor benefits. For married working men, for whom spousal and survivor benefit are most likely paid to their spouse, we find that incentives from survivor benefits to delay claiming, and from spousal benefits to claim sooner, are not influential in the work decision. For married working women, for whom spousal and survivor benefits are most likely to supplement their own benefit, we find those supplemental benefits, which provide a disincentive to continue working, are not strongly associated with their work decision.

The lack of response in both cases could either signal a lack of salience due to the complexity of these benefits or that workers place less value on benefits paid to their spouse. Limited salience would be consistent with recent evidence from the Understanding America Survey that finds limited knowledge of eligibility rules for these benefits (Perez-Arce, Rabinovich, Samek and Yoong, 2019).

Our results suggest there is room to promote retirement security by improving household decision-making. For example, delaying the collection of own benefits to build survivor benefits could serve as a mechanism that households are not currently aware of to promote the retirement security when one member has passed. Future research can inform effective outreach to near-retirement couples on how claiming decisions influence each person’s benefits while alive and in widowhood.

Our results also have implications for Social Security reform. If households that benefit from spouse and survivor benefits do not internalize them in their retirement planning through their work decisions, then are they a necessary component of Social Security in the modern era or just a surprise benefit? When these benefits were created in 1939, the majority of households were single income – 82 years later the majority are dual income households that are less likely to receive these benefits. Households that will benefit from spousal and survivor benefits do not contribute any more to Social Security than households that will not benefit. Given that Social Security’s spousal and survivor benefits amounted to $130 billion (U.S. Social Security Administration 2019), or 3.2% of total federal expenditures in 2018, that inequity among households in benefits paid could make future benefit reform a possibility.

Acknowledgements

The research reported herein was performed pursuant to a grant from the U.S. Social Security Administration (SSA) funded as part of the Retirement Research Consortium through the University of Michigan Retirement Research Center Award RDR18000002. The opinions and conclusions expressed are solely those of the author(s) and do not represent the opinions or policy of SSA or any agency of the federal government. Neither the United States government nor any agency thereof, nor any of their employees, makes any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of the contents of this report. Reference herein to any specific commercial product, process or service by trade name, trademark, manufacturer, or otherwise does not necessarily constitute or imply endorsement, recommendation or favoring by the United States government or any agency thereof.

Citations

Perez-Arce, Francisco, Lila Rabinovich, Anya Samek and Joanne Yoong. 2019. The effect of informational prompts about survivor benefits for spouses on Social Security claim intentions. Journal of Pension Economics and Finance, 1-12. doi:10.1017/S1474747219000283

Shoven, John B., and Sita Nataraj Slavov. “Does it pay to delay social security?.” Journal of Pension Economics & Finance 13, no. 2 (2014): 121-144.

Gruber, Jonathan and Wise, David. 2004. Social Security Programs and Retirement around the World: Micro-Estimation, Cambridge, MA: National Bureau of Economic Research. http://www.nber.org/books/grub04-1

U.S. Social Security Administration. 2019. Annual Statistical Supplement, 2019, Table 5a, Washington, DC. As of January 25, 2021: https://www.ssa.gov/policy/docs/statcomps/supplement/2019/supplement19.pdf

You must be logged in to post a comment.