Financial capability and economic well-being exhibit strong, positive education and income gradients. But even though high socio-economic status (SES) groups tend to be better prepared financially, it is very difficult to identify what underlying factors drive such differences. Is it different knowledge of financial products, rates of time preference, propensity to plan, motivation, self-control, cognitive ability? What is the relative importance of these factors in shaping financial decisions? Recently, studies have examined the effect of some of these underlying variables, focusing in particular on financial literacy and planning attitude. Adding to this line of work, we document the extent to which observed heterogeneity in financial decision-making and well-being within SES groups is linked to cognitive ability. For this purpose, we use data from the 2012 National Financial Capability Study (NFCS).

NFCS survey participants took computer-adaptive tests to determine their cognitive ability. These tests include (i) the number series test, where respondents are given a sequence of numbers with a blank somewhere in the sequence and asked to provide the missing value; (ii) the verbal analogies test, where respondents are shown words that make up an analogy and, based on this relationship, are asked to complete a second analogy where one word is missing; (iii) the picture vocabulary test, where respondents are shown pictures and asked to name the object they see; (iv) the abstract reasoning test, where respondents are asked to solve various problems involving abstract reasoning; and (v) the antonyms test, where respondents are shown a word and asked to type another with the opposite meaning. We combine the scores on these tests and classify individuals as having “low” cognitive ability if their total score is below the first tertile of the sample distribution and as having “normal/high” cognitive ability otherwise.

A critical component of financial capability is making ends meet. This can be measured by households’ difficulty in keeping up with monthly expenses and by how often and how much outlays exceed disposable income. The data indicate clear evidence of financial strain among American adults. Two thirds of sample households report struggling to pay their bills. About 38% spend all their disposable income and 25% regularly spend beyond that.

Difficulties to make ends meet are more pronounced among low socioeconomic status (SES) households. Yet, the data reveal striking differences by cognitive ability within education and income groups. Among respondents with high school or less and college education or more, those with low cognitive ability are about 20 percentage points more likely to report difficulty covering expenses than those with normal/high cognitive ability. Similarly, among those reporting household income less than $35,000 or more than $75,000, respondents with low cognition are 16 percentage points more likely to face difficulty covering expenses than those with normal/high cognition. Low cognitive ability is also associated with a higher tendency to spend more than disposable income, especially among high SES households. This suggests that, above and beyond education and availability of resources, cognitive ability greatly influences financial behavior.

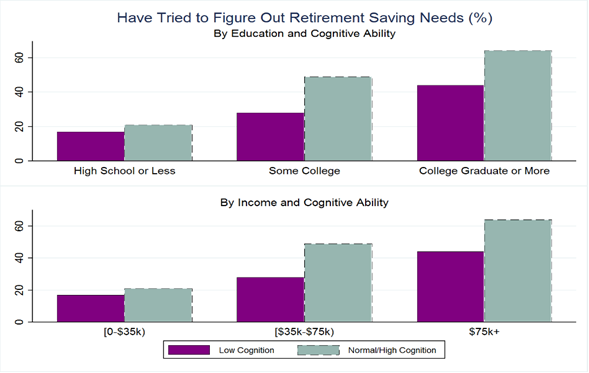

We also examine the impact of cognitive ability on financial planning, which is critical to secure economic wellbeing over the life cycle. The data reveal prominent a lack of planning attitude, as only 40% have ever thought about retirement and their savings needs. Developing an adequate retirement plan is a complicated and challenging task. It requires taking into account a variety of future, uncertain variables, including earnings, contributions rates, amount of expected Social Security and pension benefits (if applicable), investment returns and tax rules, and using this information to gauge the resources needed to sustain a certain lifestyle in retirement. The cognitive effort inherent in these computations is substantial and might discourage individuals who are not equipped with the necessary skills to successfully perform them. Figure 2 shows a strong, positive association between cognitive ability and propensity to plan for retirement within mid- and high-SES groups. The gap between individuals with low and normal/high cognitive ability is rather modest at the bottom of the income distribution. This pattern suggests that, while poor cognitive skills represent a big barrier for retirement planning, resource scarcity may be a more difficult hurdle to overcome towards setting mid- and long-term saving goals.

In order to comprehensively assess Americans’ financial capability, it is essential to understand how they borrow money and manage their debt. The most common form of unsecured debt is credit card debt. Less than half of credit card holders have always paid their balance in full in the past 12 months and about 60% have engaged in at least one behavior that results in interest charges or fees. The proportions of those who do not pay their credit card balance in full and are occasionally late with their payment is substantially larger at the bottom of the cognitive ability distribution. Also, the fraction of those who have used their credit card for cash advance is 12%, among individuals with the low cognition, and 2%, among those with the normal/high cognition.

The overall assessment of Americans’ financial capability emerging from our empirical investigation is somewhat discouraging. Within different SES groups, cognitive ability has the potential to explain a great deal of heterogeneity in financial decisions. While it is critical to gain further insight on this relationship, our results provide support for specific policies that could improve individual financial decision making among different segments of the population. These may take different forms, from financial counseling for the elderly, who are at higher risk of cognitive decline, to simplification of financial products to make it easier to use them and to compare across them. Other initiatives may target cognitive ability either directly or indirectly. Examples are memory training interventions designed to enhance episodic memory, inductive reasoning and processing speed among older adults (see the Advanced Cognitive Training for Independent and Vital Elderly) or programs promoting physical activity, nutritional habits and social interactions, which have proved to slow down the process of cognitive aging.

[1] The National Financial Capability Study (NFCS) is an ongoing survey first conducted in 2009. It is commissioned and supported by the FINRA Investor Education Foundation, in consultation with the U.S. Department of the Treasury and the President’s Advisory Council on Financial Literacy. In 2012, the NFCS survey was administered to a representative sample of 2,000 individuals selected within the RAND American Life Panel (ALP), allowing to more comprehensively document heterogeneity in financial capability across U.S. households.

You must be logged in to post a comment.